Peloton 4Q21 earnings breakdown

Peloton 4Q21 earnings breakdown

Summarising the most important points from Peloton's Q4 2021 earnings.

Quick highlights

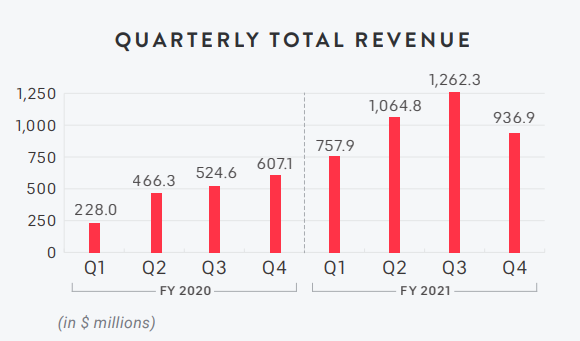

Total 4Q Revenue was $936.9 million +54% Y/Y down 25% sequentially

Connected Fitness Revenue (Hardware sales): $655.3 million +35% Y/Y

Subscription revenue: $281.6 million +132% YoY

Connected fitness activity: 134.3 million workouts +75% YoY

Average Net Monthly Connected Fitness Churn of 0.73% remains low.

Growth is slowing with Peloton providing revenue guidance of $800m for 1Q which is disappointing.

Engagement

Peloton mentioned last quarter that engagement would decline due to the summer months having an impact, with members outside more. However it seems to have dropped more than Peloton would have hoped. Peloton is expecting a return to normal seasonality now that the pandemic is coming to and end across its markets.

Profitability

Peloton will continue to invest profits back into the business to drive growth, prioritising growth over profit.

Net loss for Q4 was $(313.2) million versus net income of $89.1 million in the same period last year.

Peloton has reduced the cost of its Bike product to $1,495 - down $400. Doubling down on growth now that supply constraints have reduced.

To support growth, Peloton has invested heavily in sales and marketing. This expense was $229.3 million, and growing 172.3% YoY, representing 24.5% of total revenue versus the prior year period of 13.9%.

Tread recall

There were higher than anticipated returns of the Tread and Tread+. Peloton is recognising a higher than expected return rate which will impact profitability in the future. It also had a knock on impact on reverse logistics.

This likely means the impact to the brand, which is a long-term impact and hard to measure is higher than anticipated.

Analyst questions

One of the most insightful elements of any earnings call is the question and answer session. I’ve summarised the analyst questions and Peloton’s answers into themes.

Question: Given guidance is lower, what is the demand for Bike and Bike+. Is the price drop offensive or defensive?

Answer: Demand for Bike and Bike+ is robust. Price drop is offensive not defensive. Supply chain investments are fruitful and allow us to ship more at lower the price. Plan to is build subscriber base and increase long-term value with adjacent sales e.g. apparel. Note - Peloton believes it will increase overall revenue by lowering the price.

Question: What is the Tread gross margin?

Answer: Margin for Tread is in the low teens. Manufacturing processes have significantly improved and moving production to the US will improve margin long-term.

Question: What did you learn from Tread launches (UK and Canada) and what are the expectations for Tread and Tread+ in the US?

Answer: Learning about the experience and programming (software and content). Platform was proven in UK and Canada. Reception in Canada and UK was well received - product NPS was 84 for Tread. Tread is a strength training platform which adds a new dimension to the Peloton offering. Sales will predominantly come from existing members.

Question: Is the Bike price reduction been driven by manufacturing efficiencies?

Answer: 70-80% improvement in the cost of the Bike and Bike+. At $1,495 entry price point it will be worth sacrificing gross profit for revenue and driving growth. Conversion will uplift and it’s the appropriate trade off for long-term profitability.

Question: What should we think about the margin profile for corporate wellness?

Answer: We are still building infrastructure and we believe it’s a huge market but we are starting slow and it’s early days. Corporate wellness will allow us to obtain new customers.

Question: Are you worried about getting product to consumer through the holiday season?

Answer: We’ve built the infrastructure to support the holiday season and a large part of our business is in 2Q and 3Q. We’ve invested and we’re saving for what will be our biggest holiday season ever. Inventory is up and we’re building it to reduce lead times and diligent in our learnings from the past to execute this year.

Question: Unit capacity of close to 2 million. Are you building out the capacity and it scaling relative to 2 million units.

Answer: We’re adding subs at 50% each year. We will remain a hyper growth company for the next few years. We need to strike a balance with inventory levels. Long-term investments are in place (Ohio factory) to support capacity.

Question: Does total addressable market (TAM) and software addressable market (SAM) increase with the new lower price for Bike?

Answer: Yes, we expect an addition TAM and SAM but we haven’t re-run the analysis. The biggest factor to increase SAM and TAM is awareness. We’re making investments in marketing to solve this.

Question: What is the opportunity for Tread?

Answer: Market for Tread is higher than Bike. More runners and more treadmills exist versus stationary bikes.

Summary

Peloton continues to grow year on year but is yet to be profitable. Peloton’s long-term plan is to reinvest in marketing and R&D and profitability will likely come in calendar year 2022. Guidance for revenue is disappointing and the short-term benefits from the pandemic are not expected to continue.

If you enjoyed this newsletter, subscribe to receive future emails directly in your inbox, every week. I write analysis on Peloton and home fitness. My newsletter is free to subscribers.