Charting Peloton's progress 4Q21 update

Charting Peloton's progress 4Q21 update

Reviewing the key performance indicators (KPIs) from Peloton's 4Q21 earnings statements.

An update to my previous article, adding the latest quarterly information from 4Q21.

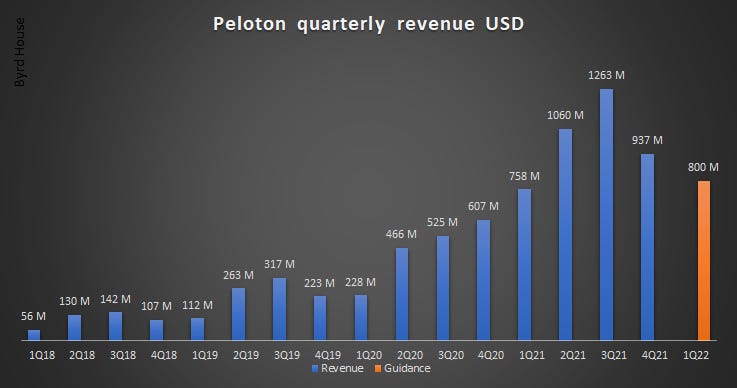

Revenue

Peloton’s revenues are slowing and the benefit from the pandemic is diminishing. Total quarterly revenue was up +54% YoY but down 25% sequentially. This is made up of hardware sales of $655.3 million +35% YoY and subscriptions of $281.6 million +132% YoY.

Revenue guidance for 1Q22 of just $800 million is significantly lower than analyst expectations and the Peloton share price has dropped 16% in the past month. It’s disappointing to see such conservative estimates.

Peloton has reduced the price of its Bike to $1,495 and this will likely increase hardware sales but naturally at lower revenues. Peloton believes it will be net positive, meaning it will sell more units overall at the lower price and therefore increase total addressable market (TAM). By providing guidance of $800m it can’t be that confident this is true. The lower price point is offensive because it grows TAM for the Peloton bike, but also defensive as it restricts competitors from gaining traction.

Profitability has also been hit significantly due to increased marketing costs. Investors will be nervous that Peloton is having to spend more on marketing to drive consideration and the increased spend means rising acquisition costs.

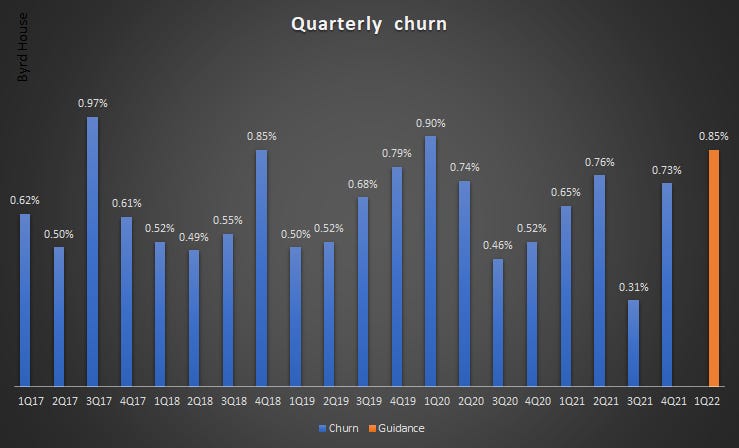

Churn

A key metric is customers cancelling their Peloton subscriptions. This is called churn and is a key measure of success. You’re always going to have a leaky bucket with customers leaving you. I believe loyalty is built on the engagement of its members. By focusing on fantastic and varied content, delivery by a wide range of exceptional instructors it’s a habit that remains. Equally, the community that’s built around Peloton means you’re more likely to feel committed.

Churn remains flat and has never increased beyond 1%. Churn is at extremely manageable levels and Peloton’s guidance expects it to stay that way.

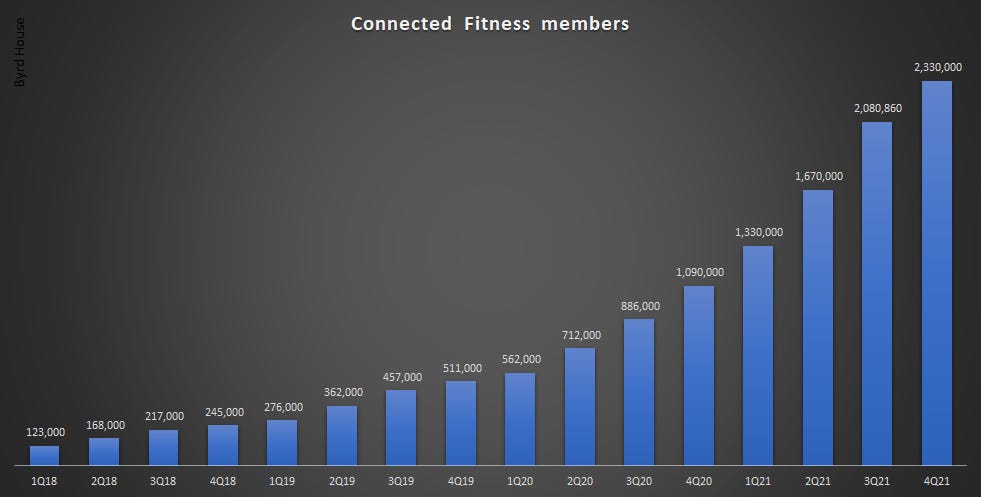

Membership

Peloton has seen its membership numbers increase slower than it had hoped. It previously stated that supply issues were a frustration and one of the reasons for the slower growth. However, these problems are now behind it and membership numbers whilst growing have slowed. Partly due to the summer months seasonality, but nevertheless increased slower than it had hoped.

Hardware subscriber growth is also slower than hoped, hitting 2.3 million members.

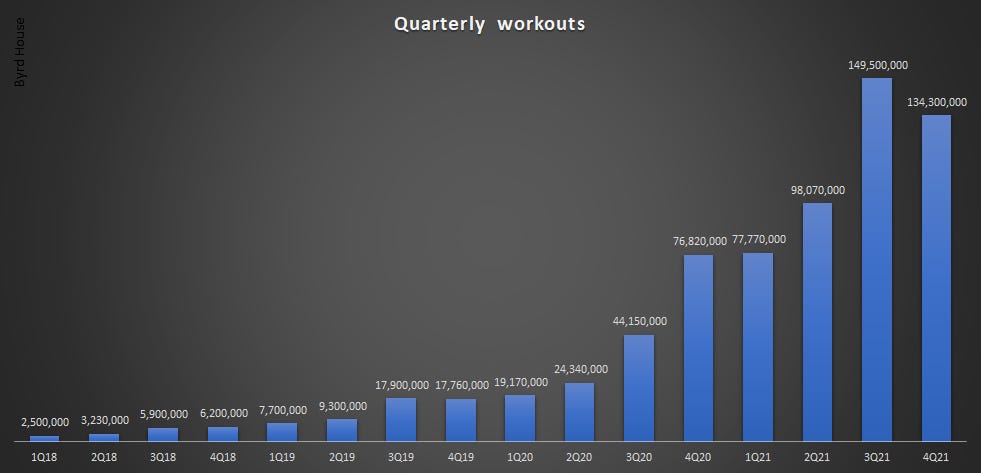

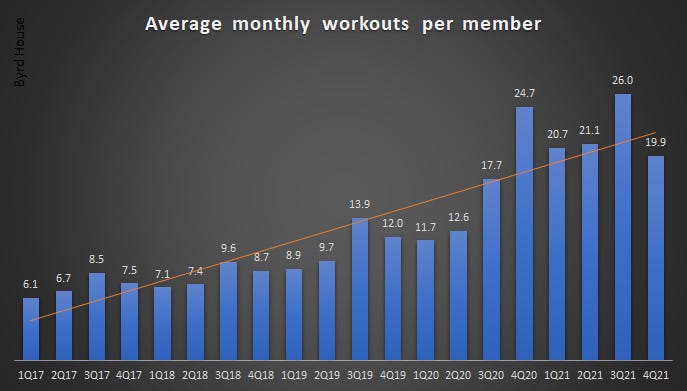

Engagement

I received some great comments on engagement from my subscribers. Peloton reports the number of workouts members have completed. This can be disingenuous as not all workouts are equal. A far better measure would be the number of minutes on the platform, per user, per month. This would provide a true reflection of engagement. If members stack four shorter workouts of around 10 minutes (40 minutes), that’s better for Peloton’s reporting than one a single workout of say an hour. Peloton even has a blog article dedicated to shorter workouts (The Benefits of Doing Multiple Short Workouts Each Day)

Peloton puts a lot of focus on this metric, but it certainly would be good to see it in minutes. It blames the warmer summer months within the quarter for a reduction in engagement and mentioned it expected a reduction in its 3Q21 earnings report.

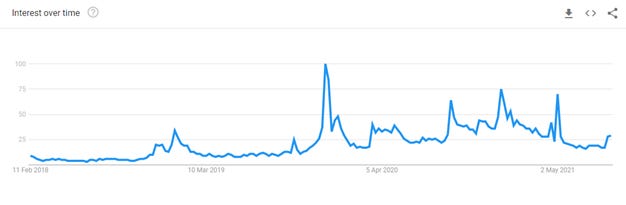

Google Trends

Searches on Google for Peloton (Exercise equipment company) are down approximately 50% from the same period last year. This again shows the benefit from the pandemic has diminished but can also be linked to the share price performance. Many investors were searching as Peloton’s share price increased significantly.

Convenience

All of the above metrics fail to understand or quantify the benefit members get from having a convenient fitness solution within their homes. Likelihood to workout is significantly increased when you don’t need to go to the gym. It’s remains the biggest benefit to owning a Peloton.

Summary

Peloton’s growth is slowly but it continues to report positive KPIs:

Revenue growth has slowed significantly and guidance expects modest YoY growth in 1Q22

Churn remains stable and guidance expects it to remain under 1%

Membership numbers continue to grow but slower than hoped